Finding any form of leading indicator for just about any market is perhaps one of the better tools at your disposal, as the anticipation and confirmation of a major shift is already present elsewhere. Correlation analysis is one of the most constant methods used by macro traders in order to asses future opportunities for this reason, as variances are sought in order to extract profit.

Of common correlations, the crude oil/currency relationship is perhaps the most widely discussed yet greatly misunderstood. USD/CAD is the most frequently discussed, as Canada is one of the highest net exporters of crude oil, yet most commonly traded. Buy why, and how these fluctuations occur is oftentimes head-scratching material for most people, so today we are going to break down this relationship in a digestible form, providing history and evidence of how these two instruments (oil, currencies) interact.

Before we get too far, let's start in a very general sense: overall, the U.S. dollar and crude oil have traditionally shared an inverse relationship. By extension, and owner of crude oil is essentially shorting the dollar and vice versa. And while trading correlations is generally considered a long-term approach, short-term value is still very much present. Shocks in one instrument have a direct impact on the other, and the lead/lag relationship will remain constant. More on this is explained below.

A Little Bit of History: The Inverse Relationship of Oil and the U.S. Dollar

The crude/anti-dollar relationship began towards the end of World War II, with the signing the Breton Woods agreement. It established the modern global financial system with the dollar serving as its foundation. From this time forward, the dollar became the central currency that was held in reserve by central banks. The result is that oil and greenback move in the opposite directions of each other.

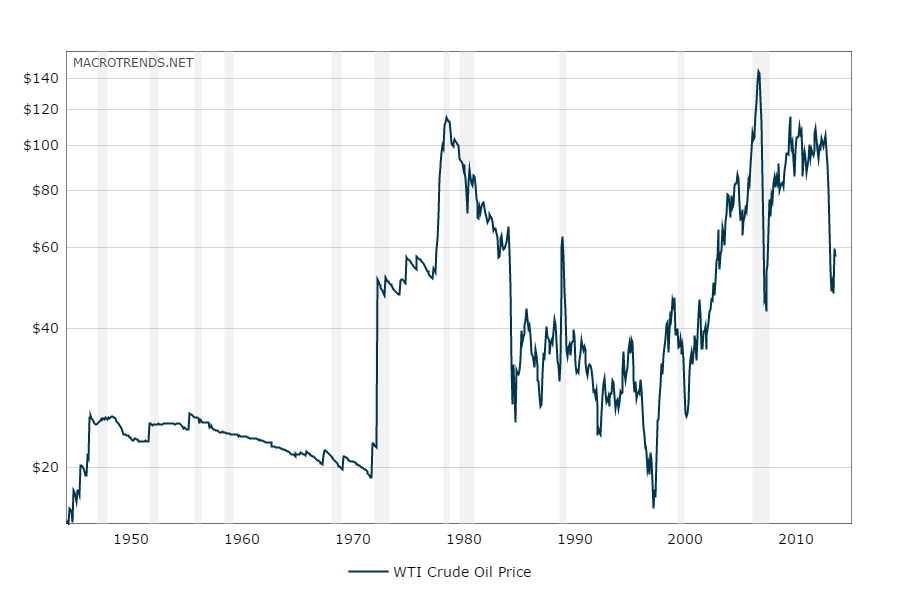

For example, after 1948 oil traded at $17.68 (on an inflation adjusted basis). These trends remained in place through 1973, when the US abandoned the gold standard and allowed the dollar to float freely against other currencies.

Over the next 7 years, oil rose to an all time high of $116.98 in late 1979, while the dollar experienced dramatic selloffs with traders moving out of the dollar and into commodities. Oil is one of the most popular, as it has always been considered a general hedge against inflation. During the same time, the dollar decreased from $103.50 to $82.47. This is when a reversal began.

A similar shift occurred in 2002, the difference being that the dollar peaked and oil bottomed. In this situation, the greenback reached a high of $115.72 (in 2002) and declined to $84.61 (by 2008). While this was happening, oil increased from $25.82 per barrel (in 2002) to an all time high of $144.51. This is illustrating the inverse relationship between the two asset classes.

What's Happening Now

In the last 12 months, these differences have become more pronounced with oil falling from $105.12 to $47.72, and the dollar steadily increasing from $68.68 to $100.31. This is in response to a stronger economic outlook for the US, comparative deteriorating conditions for much of the rest of the G10 and declining demand for commodity prices in developing economies. The extended oil supply in the United States, as well as the Saudi's refusal to cut supply was a primary driver of crude's demise.

The combination of these factors is creating a situation where dollar denominated assets are in demand. This has only lead to an accelerated selloff in oil and a rise in the value of the dollar overall.

Apples and Oranges

Over the long-term, the dollar and crude oil have been shown to inversely correlate with each other and in many instances, the dollar's price movements will lead those of oil. This is due to any number of different factors affecting the supply and demand of crude itself, actions taken by the Federal Reserve or other macro situations where the dollar is valued/devalued versus its peers.

In some cases, added amounts of liquidity with falling interest rates have had a direct impact on demand for oil. This causes prices in oil to lag the dollar. For example, in February 2002 this occurred with the Federal Reserve cutting interest rates after the September 11th terrorist attacks and wanting to restore confidence (in the wake of the Enron accounting scandal). However, oil did not begin to steadily climb upward until two months later (in April 2002).

Conversely, the dollar peaked with the Federal Reserve raising interest rates in 2005. This was partly in response to concerns that rising commodities prices were fueling inflationary pressures. The result is that the dollar reached a high of $99.20 (in 2005) and fell to $84.51 (by 2008). During this time, oil set a series of newer all time highs of $78.09. This trend continued until June 2008 when prices reached $144.51. In this case, the dollar reached its lows in March 2008 and oil followed an inverse pattern within two to three months of the shift in trends for the dollar (in June 2008).

These examples are showing how the dollar will highlight shifts in the patterns of both asset classes first. The differences are that these changes occur over the course of several months before they are realized in crude oil.

This relationship is commonly witnessed on a much shorter-term basis as well, perhaps better serving the needs of swing traders. More on this below.

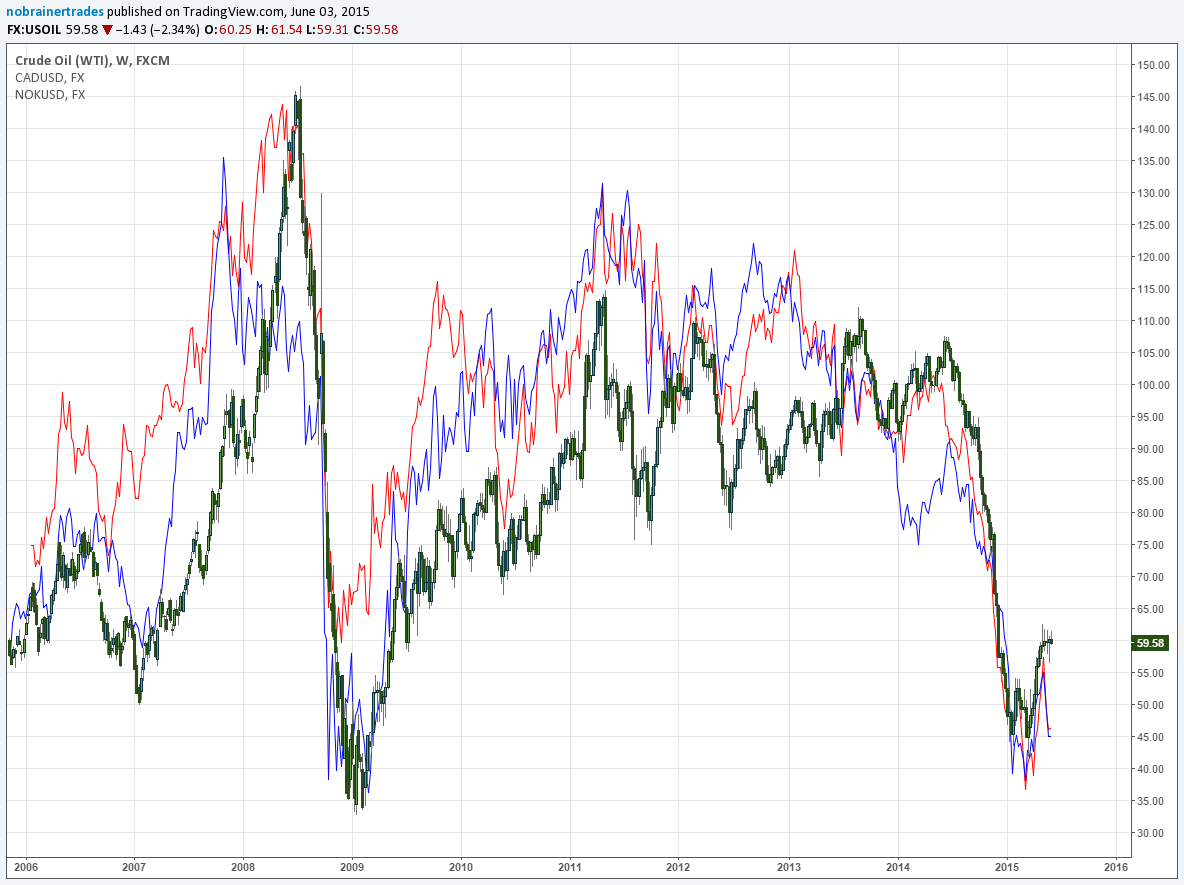

Canada (CAD) and Norway's (NOK) Tight Correlation to Crude

When we look at individual currencies having a relationship with oil, we have three primary things to consider:

1. Net exporters

2. Net importers

3. Producers

We then drill down to the most liquid of these currencies. Norway and Canada are the world's 8th and 9th largest net exporters respectively, and the only ones falling in the G10. Plotting either one of these currencies over the price of crude is going to produce an immediately clear relationship. The below chart illustrates this point, with both USD/CAD and USD/NOK inverted to better display the correlation.

Exporters are always going to be the most sensitive as the price of oil is going to have a direct impact on how much money that country is simply taking in, in relation to their overall GDP. One look at what happened to the Russian Ruble during crude's immediate downfall earlier this year makes this all the more astoundingly clear.

These are the currencies you are going to want to monitor the most in relation to this correlation overall.

So if these currencies are directly related to the price of crude and are traded against the dollar, the net effect is of course an underlying push in the other direction, against the dollar. Add this point to others mentioned above, and we equate crude as very much inversely correlated with the U.S. dollar itself.

What Do the Current Trends Signify?

Recently, the Federal Reserve announced that they will be raising interest rates at some point this year (and we will see how that one goes, as there is still a considerable amount of pressure preventing them from doing so). This is having an impact on both, as the possibility of any shifts will lead to stagflation, when interest rates are rising and the economy is lagging the historical norms.

In April 2014, these changes started with the dollar testing its lows and then moving higher. Conversely, oil reached a high of $105.12 (by June 2014). Since this time, the dollar has moved to $101.30 and oil has declined to $44.72. This is demonstrating how rising interest rates will have an underlying impact on this relationship.

Correlations and Trading Application

As with most things in trading, the biggest challenge of trading two asset classes with any correlation boils down to timing. As a general rule of thumb, currencies are largely considered the “fastest” market, largely due to the fact that everything is of course based on the value of money alone. The “price” of crude is only relative to the point of how much $1 is even worth compared to other currencies. This is only top of the fact that currencies are far more liquid and traded heavily around the clock, all year long.

There will be times when a divergence will appear, and you're going to question whether or not such a divergence is going to keep expanding or contract. A number of different strategies become available, many of which are heavily discussed in much greater detail elsewhere. The most notable include:

- Statistical arbitrage, where standard deviations are commonly used to determine how far apart these instruments really are to one another in relation to x values in the past. In a stat. arb. strategy, a long and short position is typically applied on a volatility-adjusted basis. This is done to take advantage of the variance in correlation (ie short crude, short USD/CAD effectively long CAD) and to seek profit from the two converging. A “synthetic” instrument is calculated in order to determine this (a spread between crude and CAD). There are many, many variations of statistical arbitrage, but this is the most common example.

- Naked longs or shorts in the “lagging” instrument. As an example, both CAD and NOK are trading somewhat significantly below crude oil currently. A short in crude would seek a convergence to the two currencies.

Our recommendation is to keep it simple. While the dollar is going to have the most significant impact overall, the more macro you get, the less sensitive your rates become overall. Focus on your high-exporting nations first and foremost. These are the sovereigns relying on / are the most sensitive to the price of crude and whose overall value of currency tends to lead the pack. They are as follows:

How This All Lines Up

Recent charts are showing how oil is currently going through a bear rally. This is expected given the scope of the decline the commodity experienced since June of 2014. Based on what we know, the current levels of the dollar are indicating that prices could move slightly lower. Should the dollar maintain its upward trajectory, crude is likely to experience a second wind in relation to decline itself. You would target a mean between these two, or essentially where the correlation once again becomes intact.

The most important underlying assumption is to watch is the way the dollar reacts. This is because it will normally lead any moves in oil by a term relative to the recent price action. If the underlying trend shifts, this could be a sign that the commodity may have bottomed and is starting to rise. Those who follow this strategy can objectively analyze what is happening and identify strong entry points.

Technical breaks on the dollar, not accompanied with breaks on crude, can be effective. The chart below demonstrates two separate instances where the two were floating in a relative range. The dollar broke out and retested local trendlines while crude took several days to accompany the movement itself.

And In The End….

Correlation analysis is a very common strategy institutions always have an will continue to use to decrease their risks and enhance their total returns. The key for successfully trading it requires ensuring that both instruments are diverging from a norm, with no major catalyst pull on either one or the other, without the other. This means watching how each one is reacting in comparison with their highs and lows. Those who are able to take advantage of these disparities when they are first emerging will realize larger overall returns.

In the case of the US dollar and oil, an inverse relationship continues to exist. The two will trade in opposite directions each other and are influenced by a plethora of monetary / economic factors. This causes them to move in patterns with the US dollar showing inverse correlation first. Then, within relative short order, oil is confirming the underlying trends by moving in the opposite direction.

As with anything, keep your relationships relatively simple. While we have spent a fair amount of time outlining several different factors attributing to the rise and decline of crude and currencies, every correlation needs to be respected for what it is at any given moment. Observation and screentime are always your best friend when it comes to virtually any intermarket relationship, as history does indeed change with driving factors themselves.

For more:

List of exporters/importers, production, consumers and reserves: http://www.eia.gov/beta/international/index.cfm?topl=imp

Charts and other correlation analysis: https://www.tradingview.com and http://macrotrends.net and https://www.quandl.com/

Stat arb: http://www.nasdaq.com/article/dont-be-fooled-by-the-fancy-name-statistical-arbitrage-is-a-simple-way-to-profit-cm254669 and http://en.wikipedia.org/wiki/Statistical_arbitrage

This post was a co-written by Chris Seabury, a freelance journalist, and NBT.